Go figure. The circumstance is a lot more complicated, so consider this is an initial lesson on a very intricate topic. Suggestion: Mortgage rates can rise extremely rapidly, however are typically lowered in a sluggish, calculated way to secure mortgage lending institutions from rapid market shifts (how many mortgages can one person have). That incredibly low advertised home loan rate sure appearances goodBut be sure to take a look at the great printYou probably have to be an A+ borrowerAnd you may require to pay discount rate points tooAlso note that the par rate you see promoted on TV and the web typically do not consider any home loan pricing modifications or costs that could drive your actual interest up considerably.

If your deposit or credit rating isn't that high, or your house equity is low, your home mortgage rate may creep higher also. Tenancy and property type will also drive rates higher, presuming it's a 2nd house, financial investment property, and/or a multi-unit residential or commercial property (what is the current index for adjustable rate mortgages). So expect to pay more if that's the case.

There are likewise loan quantity restrictionspricing can change depending on if the mortgage is conforming or jumbo. Normally, month-to-month payments are higher on the latter, all else being equal. To put it simply, YOU and your residential or commercial property matter as well. A lot!If you're a risky debtor, at least in the eyes of potential mortgage lenders, your home loan rate might not be as low as what you see marketed.

At the customer level, the most significant consider determining the rate of a home mortgage is usually credit report. Among the most important elements that you can manage is your Discover more here credit history, so if you can a minimum of get a handle on that and work to keep your scores above 760, your pricing should be optimal, all else being equivalent.

There are loan calculators that will tell if paying points make sense depending on your scenario, the length of time you prepare to remain in the house, and so on. Rates can likewise differ considerably based upon how much a specific lending institution charges to originate your loan. So the last rate can be manipulated by both you and your loan provider, no matter what the going rate takes place to be.

Last but not least, note that there are a range of different loan programs offered with different rate of interest. Are we talking about a 30-year set rate or a variable-rate mortgage, the latter of which will have a lower interest rate. Loan type and loan quantities can play a big role here. Below are Freddie Mac's, upgraded weekly every Thursday morning.

An Unbiased View of Why Do Mortgage Companies Sell Mortgages

The data is gathered Monday through Wednesday, so they aren't always going to match up with today's home loan rates if rates increased or fell from then till now. Consider this a starting point:30- Year Fixed * 2. 71% 2. 71% 3. 73% 15-Year Fixed * 2. 26% 2. 26% 3. 19% 5/1 ARM2. 79% 2. 86% 3. 36%- Home mortgage rates are presently trending -* represents a record lowSince 1971, Freddie Mac has conducted a weekly survey of consumer home loan rates.

These averages do not use to government house loans like VA loans or an FHA mortgage. The numbers are based upon quotes offered to "prime" customers, those with high credit report, meaning best-case prices for the a lot of part. I think the property enter the study is for a one-unit main residence too, so anticipate a rate rise if it's a holiday house or rental property, or multi-unit home.

To put it simply, your home loan rate might differ the national average for any variety of factors, but if your mortgage is quite run of the mill, you may anticipate rates to be comparable. As you can see, 30-year set mortgage rates are the most pricey relative to the 15-year fixed and select adjustable-rate home mortgages.

So you pay a premium for the stability and absence of danger, and the chance to refinance if rates take place to decrease. Rates on the 15-year repaired are substantially less expensive, but you get half the time to pay it off, meaning larger regular monthly payments and a lot less interest paid.

25%) below the 30-year fixed. The shorter term means you'll also save a load on interest. Rates on ARMs are marked down at the start because you just get a restricted set period prior to they become adjustable, at which point they usually increase. Grab a home mortgage calculator and cost out various loan types to see what makes one of the most sense for your scenario.

If your specific loan circumstance is higher danger, whether it's a higher LTV and/or a lower credit report, it will most likely be priced higher. If you're trying to find current mortgage rates of interest, you can look at these weekly averages to see both the direction of rates and the estimate to a minimum of get an estimate of what you might get at any offered time.

Fascination About What Are Today's Interest Rates On Mortgages

71% per Freddie MacPreviously it had been as low as 2. 72% during the week ended November 25th, 2020The 15-year fixed also hit its all-time low of 2. 26% on December 3rd, 2020During the week ending December 3rd, 2020, 30-year set home mortgage rates struck new lowest levels. The popular 30-year repaired was up to 2.

72%, per Freddie Mac, the most affordable point since tracking started all the method back in 1971. Formerly, it had been as low as 2. 72% during the week ended November 25th, 2020. Up until now, there have been 14 brand-new record lows set for mortgage rates in 2020. The 15-year set hit a record low of 2.

It had actually previously been as low as 2. 28% throughout the week ended November 25th, 2020. Its floor was 2. 56% during the week ended May second, 2013 before reaching these current brand-new all-time lows numerous times in 2020. During the same week back in 2013, the $15/1 ARM also strike its all-time record low of 2.

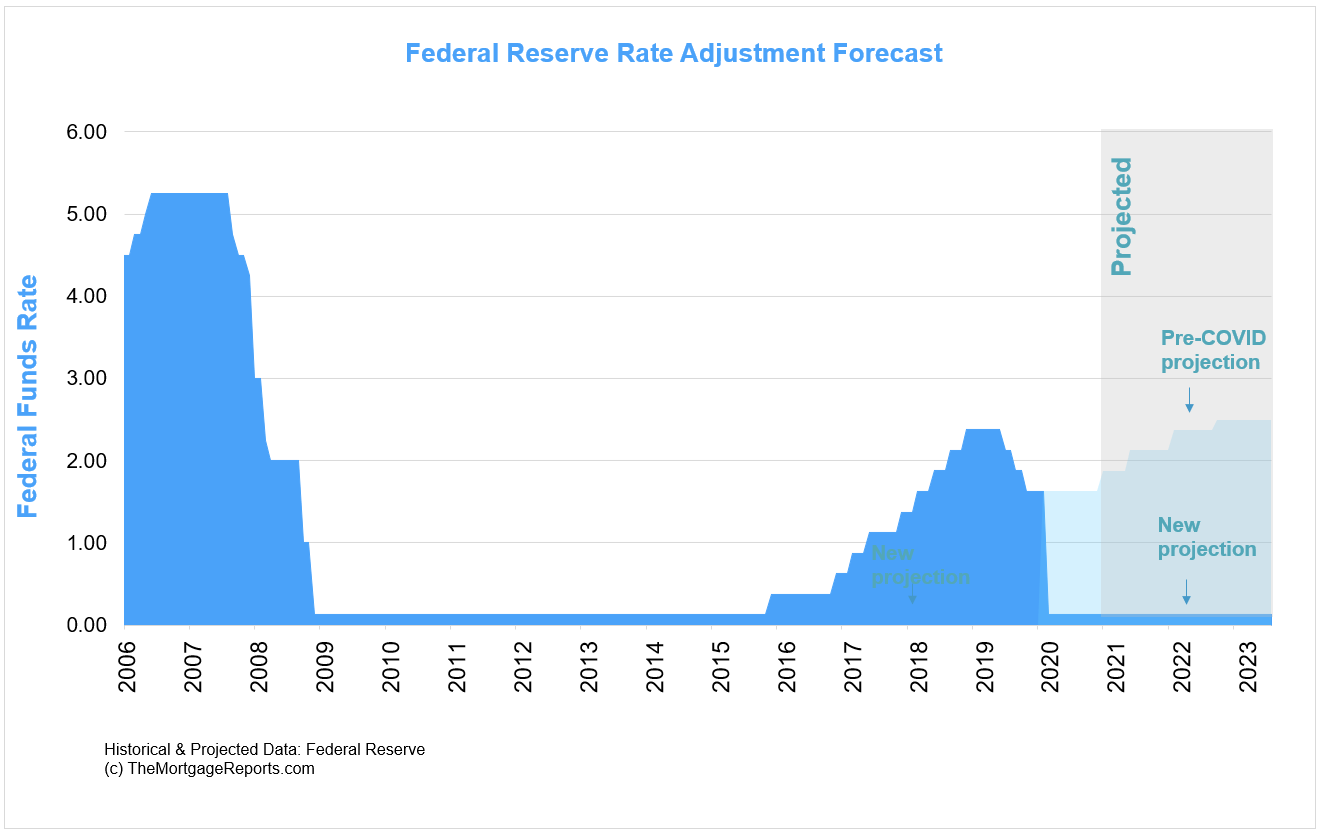

Finally, the 1 year ARM was up to 2. 41% throughout the week ended April 10, 2014, its lowest point on record because 1984. The majority of economic experts do not see rates falling back to these lows again, though anything is possible if the economy warrants such check here a move. Spoiler alert, rates hit brand-new lows!Wondering if mortgage rates are going up or down in 2020 and the year after? Wonder no Have a peek at this website longer.

Take them with a grain of salt since they're not necessarily precise, just projections for future rate motion. Fannie Mae3. 6% 3. 6% 3. 6% 3. 5% 3. 6% Freddie Mac3. 8% 3. 8% 3. 8% 3. 8% 3. 8% MBA3. 7% 3. 7% 3. 7% 3. 7% 3. 8% NAR3. 7% 3. 7% 3. 8% 3. 8% 4. 0% As you can see, mortgage rates are predicted to remain low in 2020.

Naturally, it will vary a little depending on which anticipate you think. Home mortgage rates are expected to stay in the mid-to-high 3% realm in 2020, which ought to be welcome news to the majority of. I have actually simply released 2020 mortgage rate predictions for those searching for a more in-depth assessment. Find out more: What mortgage rate can I anticipate!.

Some Known Factual Statements About How Do Banks Make Money On Mortgages

?.!?. NOTICE: This is not a commitment to lend or extend credit. Conditions and restrictions might apply. All house loaning items, including home mortgage, home equity loans and home equity lines of credit, go through credit and collateral approval. Not all house financing products are available in all states. Risk insurance coverage and, if relevant, flood insurance are required on security property.